Your payment will increase if rates of interest go up, however you might see lower needed regular monthly payments if rates fall. Rates are typically fixed for a number of years in the beginning, then they can be changed annually. There are some limitations as to just how much they can increase or decrease.

Second home mortgages, also referred to as home equity loans, are a method of borrowing versus a home you currently own. You might do this to cover other costs, such as financial obligation combination or your kid's education expenses. You'll include another mortgage to the property, or put a new very first home loan on the home if it's settled. The payment quantity for months one through 60 is $955 each. Payment for 61 through 72 is $980. Payment for 73 through 84 is $1,005 - reverse mortgages how they work. (Taxes, insurance coverage, and escrow are additional and not included in these figures.) You can determine your costs online for an ARM. A third optionusually reserved for wealthy home buyers or those with irregular incomesis an interest-only home mortgage.

It may also be the best option if you expect to own the house for a fairly brief time and plan to sell before the bigger month-to-month payments begin. A jumbo mortgage is typically for amounts over the adhering loan limit, currently $510,400 for all states except Hawaii and Alaska, where it is greater.

Interest-only jumbo loans are also available, though generally for the extremely wealthy. They are structured likewise to an ARM and the interest-only period lasts as long as 10 years. After that, the rate adjusts yearly and payments go toward paying off the principal. Payments can increase substantially at that point.

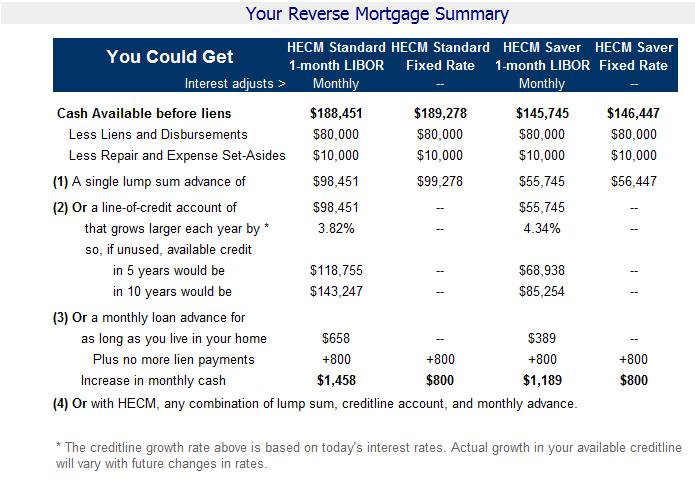

The 10-Second Trick For How To Reverse Mortgages Work

These expenses are not repaired and can fluctuate. Your loan provider will detail extra expenses as part of your home loan contract. In theory, paying a little extra monthly toward minimizing principal is one way to own your house quicker. Financial specialists recommend that exceptional financial obligation, such as from credit cards or student loans, be settled first and savings accounts need to be well-funded before paying extra every month.

For state returns, nevertheless, the reduction differs. Contact a tax professional for particular recommendations concerning the certifying guidelines, especially in the wake of the Tax Cuts and Jobs Act of 2017. This law doubled the basic deduction and reduced the quantity of home mortgage interest https://www.globenewswire.com/news-release/2020/06/25/2053601/0/en/Wesley-Financial-Group-Announces-New-College-Scholarship-Program.html (on new home mortgages) that is deductible.

For numerous households, the right house purchase is the very best way to develop an asset for their retirement nest egg. Likewise, if you can avoid cash-out refinancing, the house you purchase age 30 with a 30-year set rate home loan will be totally settled by the time you reach typical retirement age, providing you an affordable place to live when your revenues reduce.

Participated in in a sensible way, house ownership stays something you must think about in your long-lasting financial preparation. Understanding how home mortgages and their rates of interest work is the very best method to guarantee that you're constructing that possession in the most financially advantageous method.

The Main Principles Of How To Reverse Mortgages Work

A home loan is a long-term loan created to help you purchase a home. In addition to repaying the principal, you likewise need to make interest payments to the lender. The house and land around it act as collateral. But if you are looking to own a home, you need to understand more than these generalities.

Home mortgage payments are comprised of your principal and interest payments. If you make a down payment of less than 20%, you will be needed to secure private mortgage insurance, which increases your monthly payment. Some payments also include realty or real estate tax. A borrower pays more interest in the early part of the mortgage, while the latter part of the loan favors the principal balance.

Home loan rates are regularly discussed on the evening news, and speculation about which direction rates will move has end up being a basic part of the monetary culture. The modern-day home mortgage entered being in 1934 when the governmentto help the nation got rid of the Great Depressioncreated a mortgage program that minimized the required down payment on a house, increasing the amount prospective house owners might obtain.

Today, a 20% down payment is desirable, mostly due to the fact that if your down payment is less than 20%, you are required to get personal home loan insurance coverage (PMI), making your monthly payments higher. Desirable, nevertheless, is not necessarily achievable. how do points work in mortgages. There are home mortgage programs readily available that permit substantially lower down payments, however if you can handle that 20%, you certainly should.

Some Known Incorrect Statements About How Do Mortgages Work When You Move

Size is the quantity of money you borrow and the term is the length of time you need to pay it back. how do buy to rent mortgages work. Usually, the longer your term, the lower your month-to-month payment. That's why 30-year mortgages are the most popular. Once you understand the size of the loan you require for your new home, a home mortgage calculator is a simple method to compare mortgage types and numerous lenders.

As we take a look at them, we'll utilize a https://www.youtube.com/channel/UCRFGul7bP0n0fmyxWz0YMAA $100,000 home mortgage as an example. A portion of each home mortgage payment is devoted to repayment of the principal balance. Loans are structured so the amount of primary returned to the debtor starts out low and increases with each home mortgage payment. The payments in the first years are used more to interest than principal, while the payments in the last years reverse that situation.

Interest is the loan provider's benefit for taking a risk and lending you money. The rate of interest on a home loan has a direct influence on the size of a mortgage payment: Higher interest rates suggest higher mortgage payments. Greater rates of interest usually decrease the quantity of cash you can obtain, and lower rate of interest increase it.

The exact same loan with a 9% rate of interest lead to a monthly payment of $804.62. Realty or property taxes are examined by federal government companies and used to money public services such as schools, authorities forces, and fire departments. Taxes are determined by the government on a per-year basis, but you can pay these taxes as part of your monthly payments.