If you stay in your house for longer than 67. 6 months, then you're much better off for having bought the points because you have actually offseted your initial $2,500 investment and you continue to enjoy payments that are $37 lower on a monthly basis. If you remain in your home and keep settling your home mortgage for thirty years, you'll pay a total of $13,325 less in interest.

That's a substantial quantity of savings-- however of course you just recognize it if you stay in your house. If your future is not specific and you do not think you'll be remaining long enough to break even, you might not wish to incur the initial expense of purchasing the point - how do second mortgages work in ontario. The longer you intend on living there, the much better the chance that mortgage points will be worth it. With a home mortgage calculator, you can identify exactly how long that is and whether or not mortgage points deserve it in your circumstance. In addition, you do require to weigh in tax benefits, the schedule of outside financial investments, and your cash on hand.

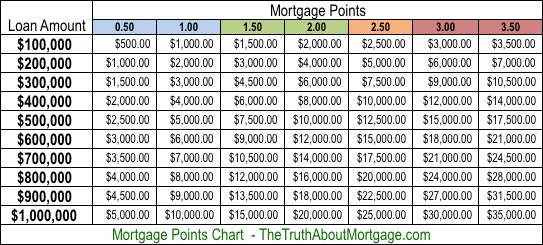

Usually, the cost of a home mortgage point is $1,000 for every single $100,000 of your loan (or 1% of your overall mortgage quantity). Each point you acquire reduces your APR by 0. 25%. For example, if your rate is 4% and you purchase one point, your APR rate would go down to 3.

Because your rate is lower, you will conserve a little bit on each of your home loan payments. Ultimately, gradually, those savings will increase and equivalent and exceed the amount you needed to spend for the discount rate. This is referred to as the break-even point. Home mortgage calculators can assist you determine precisely where that break-even point is.

8 Easy Facts About How Does Chapter 13 Work With Mortgages siriusxm get started now Explained

If you keep your house longer than the break-even point, you'll start to understand some savings. Keep in mind, though, that all other conditions stay the exact same. Many would argue that you have to likewise compute the cash you might have earned over that period by putting the cash you invested in points in another type of investment.

( the focus of this story) lower the rate of interest on your loan and decrease your monthly payments. Home mortgage points offer you the choice to decrease your rate of interest and reduce your regular monthly home loan payments. There are 2 kinds of these points: discount points and origination points. Discount points are a form of prepaid interest that you can acquire to lower your rate of interest.

These also assist decrease the rate of interest on your mortgage. In a lot of cases, you'll pay a charge equal to 1% of the home mortgage amount for each discount poinot. This fee is normally paid directly to your lender or as part of a fee bundle. A lot of lending institutions provide the choice for property buyers to purchase home loan points, though they are not required to.

Usually, this is capped out around four or 5 points. Some lenders will let you purchase in increments, so you might not need to buy whole points if you're searching for a more tailored fit. Home mortgage points may be tax-deductible, depending on whether you satisfy the criteria laid out by the IRS.

The Ultimate Guide To How Mortgages Subsidy Work

While the majority of people will have the ability to deduct home loan points over the life of the loan, you should satisfy a number of particular requirements to subtract them all during the very first year. These are plainly set out on the IRS website. 4% rate of interest with no mortgage points 3. 875% rate of interest with 1 point4%, No points$ 477.

513.875%, 1 point$ 467. 38$ 168,257. 40 N/A$ 10. 04$ 3,612. 11If you pay 1 point, which will cost you $1,000 nashville xm radio on a $100,000 home mortgage (keep in mind, each point expenses 1% of your home mortgage amount) to get the 3. 875% rate, you lower your month-to-month payments by about $10. That suggests it would take 100 month-to-month payments, or more than 8 years, to recoup the in advance expense of that point - how adjustable rate mortgages work.

do you really plan to remain in your house for thirty years? And offering or re-financing prior to the break-even point implies you'll in fact wind up paying additional interest on the loan. Richard Bettencourt, a mortgage broker in Danvers, Massachusetts, and former president of the Association of Mortgage Professionals, says paying home mortgage points generally isn't a great financial move." The only way I see a point making good sense is for that rarity of the person who states, 'I'm going to make all 360 payments (on a 30-year home mortgage) and never ever move,'" he said.

Another way to look at home loan points is to think about how much cash you can manage to pay at the loan-closing table, states Mark Palim, vice president of applied financial and real estate research for Fannie Mae, a government-owned company that purchases mortgage financial obligation." If you consume a few of your cost savings towards prepaying your interest, that makes your payment lower on a month-to-month basis, you have less savings if the hot water heater breaks," he stated.

What Does How Do Mortgages Work In Portugal Mean?

If you know you remain in your house for the long haul, you may profit of lower regular monthly home mortgage payments for the next couple of decades. On the other hand, home loan points most likely aren't worth it if you 'd be utilizing a big portion of your savings to purchase them. Decreasing your month-to-month payments by a small quantity doesn't rather make sense if you 'd need to compromise your emergency situation fund to do it particularly if you're not dedicated to remaining in your home for the next thirty years.

If you're preparing on remaining in your home longer than the break-even point, you will see cost savings. If those cost savings surpass what you might get in outside investment, then home mortgage points will certainly deserve it. In addition, you ought to consider the requirement for capital to acquire mortgage points. When you buy a home, you need to pay for lots of things like the deposit, closing expenses, moving expenses and more.

Home loan discount points are all about playing the long video game. Usually speaking, the longer you prepare to own your home, the more points can help you save money on interest over the life of the loan. There's nobody set limit on the number of home mortgage points you can buy. However, you'll seldom find a lender who will let you buy more than around 4 home mortgage points.